Every Indian who sends money abroad, books a foreign trip, pays tuition fees overseas, or trades in international stocks operates under one law: the Foreign Exchange Management Act, 1999. Most travellers never read it. But FEMA shapes how much you can send out of India, where you can hold foreign currency, what you must declare, and how every authorised forex dealer processes your transactions.

FEMA is India’s foreign exchange law, administered by the RBI, that governs every cross-border transaction. It permits resident Indians to remit up to USD 250,000 per financial year under LRS. From April 2026, TCS rates range from 0% to 20% depending on remittance purpose.

Understanding the basics matters because FEMA quietly shapes everything from a forex card load to whether you must file Form A2 at the bank. This guide covers what the law is, what it permits, what it restricts, and where it intersects with everyday foreign exchange needs.

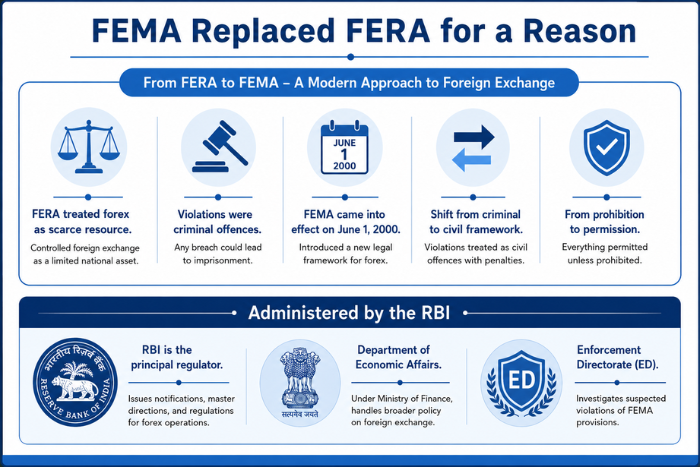

FEMA Replaced FERA for a Reason

The Foreign Exchange Regulation Act of 1973 treated foreign exchange as a scarce national resource and any violation as a criminal offence. By the late 1990s, India’s post-liberalisation economy needed a different framework. FERA was rewritten as FEMA, which came into effect on June 1, 2000.

The shift was philosophical. FERA criminalised; FEMA civilized. Where FERA presumed guilt on the accused, FEMA treats most violations as civil offences punishable by penalty rather than imprisonment. The law moved from “everything is prohibited unless permitted” to “everything is permitted unless prohibited.”

Administered by the RBI

The Reserve Bank of India is the principal regulator. The RBI issues notifications, master directions, and regulations that govern day-to-day forex operations. The Department of Economic Affairs under the Ministry of Finance handles broader policy. The Enforcement Directorate investigates suspected violations.

Current Account vs Capital Account Transactions

FEMA splits all forex transactions into two categories. Understanding this split is the foundation of every other FEMA rule.

Current Account Transactions

These cover routine cross-border payments: foreign travel, education, medical treatment, gifts, business trips, family maintenance, and import-export payments. Most current account transactions are freely permitted up to defined limits, with documentation but no prior approval needed for standard purposes.

Capital Account Transactions

These involve creating or extinguishing assets or liabilities outside India: buying foreign property, holding foreign securities, taking foreign loans, or making overseas investments. Capital account transactions are more regulated; some require prior RBI approval, others fall under permitted routes with defined caps.

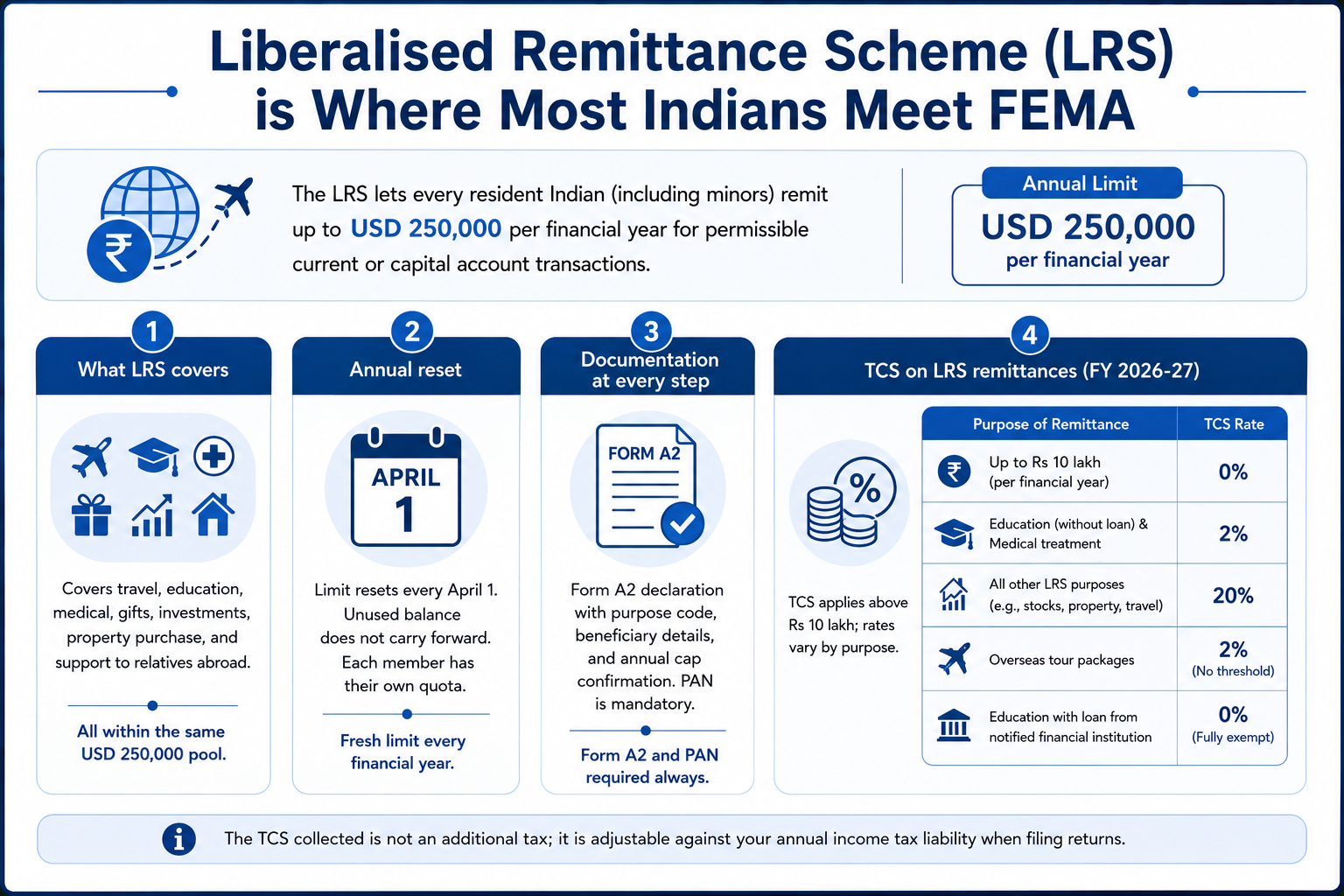

Liberalised Remittance Scheme (LRS) is Where Most Indians Meet FEMA

The LRS is the single FEMA provision that affects regular travellers most directly. Introduced in 2004 at USD 25,000, the limit was raised in stages to its current level of USD 250,000 per financial year. The scheme permits every resident Indian, including minors, to remit this amount for any permissible current or capital account transaction.

1. What LRS covers

The annual limit applies to combined spends: foreign travel, education abroad, medical treatment, gifts to relatives outside India, investments in foreign stocks, purchase of foreign property, and maintenance of close relatives abroad. All of these draw from the same USD 250,000 pool.

2. Annual reset

The limit refreshes every April 1 with the new financial year. Unused balance does not carry forward. Each family member has their own quota, which effectively multiplies the household cap when used in coordination.

3. Documentation at every step

Every LRS transaction requires a Form A2 declaration through your authorised dealer. The form captures the purpose code, the beneficiary details, and confirms you have not breached the annual cap. PAN is mandatory.

4. TCS on LRS remittances (FY 2026-27)

The TCS regime was updated by the Finance Act 2026 read with the Income Tax Act 2025, effective April 1, 2026. Remittances up to Rs 10 lakh per financial year attract zero TCS regardless of purpose. Above Rs 10 lakh, the rate depends on the purpose of remittance: 2 percent for education (without loan) and medical treatment; 20 percent for all other LRS purposes including foreign stock investments, property purchases, and general travel; and a flat 2 percent with no threshold for overseas tour packages.

Education remittances funded through a loan from a notified financial institution are fully exempt at 0 percent. The TCS collected is not an additional tax; it is adjustable against your annual income tax liability when filing returns.

Authorised Dealers Run the System

You cannot send money abroad directly. Every cross-border forex transaction in India routes through an Authorised Dealer (AD), which is an entity licensed by the RBI to deal in foreign exchange.

The categories are layered. AD Category-I banks are authorised for all forex transactions including capital account. AD Category-II entities, including most non-bank money changers, are authorised for non-trade current account transactions. Full-Fledged Money Changers (FFMC) are authorised for purchase and sale of foreign currency notes and traveller’s cheques.

Every time you load a forex card, send a wire transfer, or convert rupees to foreign currency, you are operating through an AD, even when the transaction feels like a simple online click.

Penalties Under FEMA Are Civil

FEMA violations are handled through adjudication, not criminal courts in most cases. The penalty structure is straightforward.

For violations where the amount can be quantified, such as exceeding the LRS cap, the penalty is up to three times the amount involved. For procedural violations where the amount cannot be quantified, the penalty is up to Rs 2 lakh. If the breach continues after the initial order, an additional penalty of up to Rs 5,000 per day applies for the period the contravention continues.

Most FEMA violations can also be compounded by paying a settlement amount to the RBI, which closes the matter without formal adjudication.

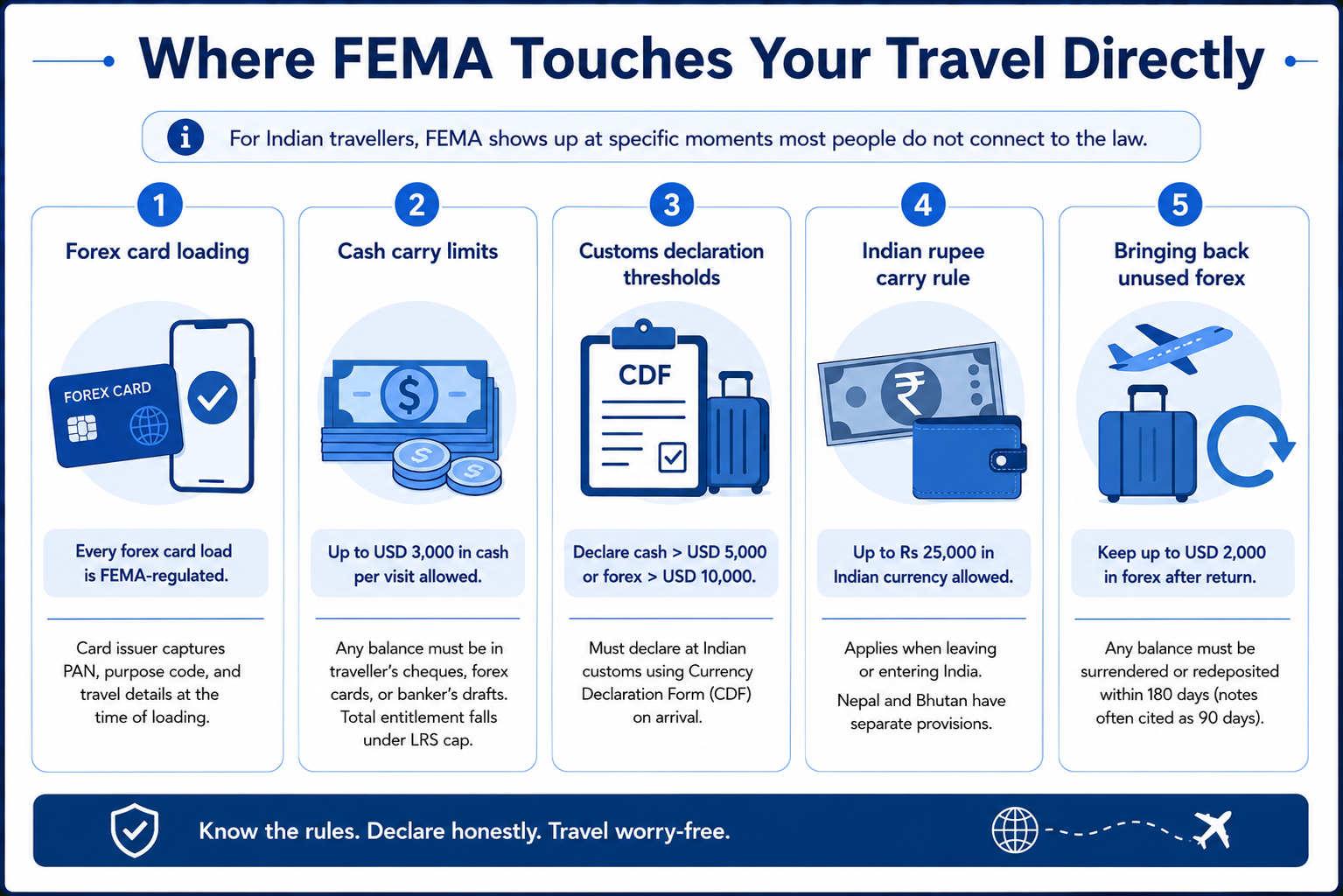

Where FEMA Touches Your Travel Directly

For Indian travellers, FEMA shows up at specific moments most people do not connect to the law.

1. Forex card loading

Every forex card load is a FEMA-regulated transaction. The card issuer captures your PAN, purpose code, and travel details to comply with reporting requirements at the time of loading.

2. Cash carry limits

You can carry foreign currency notes and coins of up to USD 3,000 or equivalent per visit. Any balance must be carried in the form of traveller’s cheques, forex cards, or banker’s drafts. Total foreign exchange entitlement for a private visit falls under the LRS cap.

3. Customs declaration thresholds

Foreign currency in cash above USD 5,000, or total foreign exchange (cash plus traveller’s cheques) above USD 10,000, must be declared at Indian customs using the Currency Declaration Form (CDF) on arrival.

4. Indian rupee carry rule

Resident Indians can carry up to Rs 25,000 in Indian currency when leaving or entering India. Travel to Nepal and Bhutan has separate provisions.

5. Bringing back unused forex

A resident can retain foreign currency notes and traveller’s cheques up to USD 2,000 in aggregate after returning. Any balance must be surrendered to an authorised dealer or redeposited within 180 days of return (currency notes are often cited as 90 days).

A Compliant Forex Solution Removes the Friction

The cleanest way to stay FEMA-compliant on a foreign trip is to use a regulated provider that handles documentation, reporting, and limits at the source rather than scrambling at the airport.

The BookMyForex Multicurrency Forex Card is issued under full RBI compliance, with every load processed through an authorised dealer route. LRS reporting is built into the loading workflow, the purpose code is captured automatically, and the card stores multiple currencies at locked-in interbank rates.

Live interbank rates at loading eliminate the spread that airport counters and credit cards quietly add. Zero issuance, reload, or annual charges keep the cost structure clean. Free international ATM withdrawals reduce the cash component you need to carry, which keeps you well within FEMA’s cash carry limits. The in-app reload feature lets you top up while travelling without breaching any reporting requirement.

FEMA is not a barrier; it is the framework that lets foreign exchange work for Indian travellers in the first place. Knowing how the law works helps you plan trips, education spends, and overseas investments without surprises at the bank counter or the airport. Start every trip with a clear forex plan and the regulations stop being a worry.

About the Author

Kshitij Pandey is the Content Manager at BookMyForex with over 7 years of experience in content marketing, blogging, and social media strategy. He has worked extensively on building engaging campaigns and informative resources that help users understand forex, international money transfers, and travel-related financial services.