You send exactly USD 1,000 to a relative abroad, but only USD 975 lands in their account. Nobody stole the rest. It was quietly deducted by a chain of banks that never appear on your receipt, under a line item most senders have never heard of: the Nostro charge. On cross-border transfers, your money does not travel in a straight line, and every stop along the way can cost you.

Nostro charges ($15–$50) are deducted mid-transit by intermediary banks routing money abroad, leaving recipients with less. Even if you opt to bear all fees, the beneficiary’s bank may still deduct an inward remittance charge, so the exact amount received isn’t guaranteed.

This guide explains what a Nostro account is, why these charges appear, how they differ from your bank’s own transfer fee, and how to structure a transfer so the recipient receives the full amount.

What a Nostro Account Actually Is

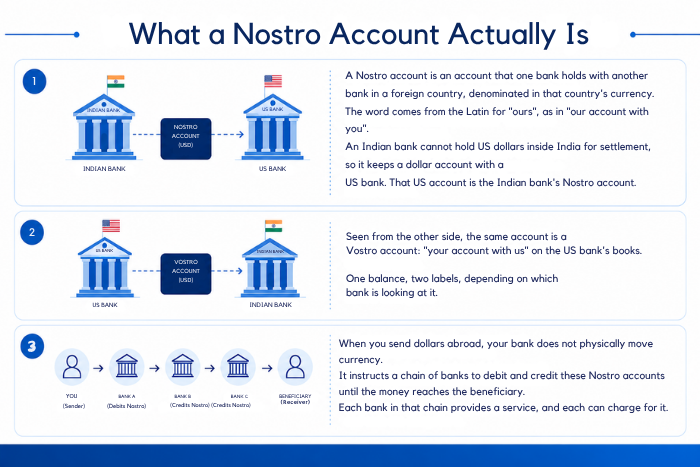

A Nostro account is an account that one bank holds with another bank in a foreign country, denominated in that country’s currency. The word comes from the Latin for “ours”, as in “our account with you”. An Indian bank cannot hold US dollars inside India for settlement, so it keeps a dollar account with a US bank. That US account is the Indian bank’s Nostro account.

Seen from the other side, the same account is a Vostro account: “your account with us” on the US bank’s books. One balance, two labels, depending on which bank is looking at it.

When you send dollars abroad, your bank does not physically move currency. It instructs a chain of banks to debit and credit these Nostro accounts until the money reaches the beneficiary. Each bank in that chain provides a service, and each can charge for it.

Why Nostro Charges Appear on a Transfer

International transfers rarely run bank to bank directly. If your bank has no direct relationship with the recipient’s bank, the money passes through one or more intermediary banks that do hold accounts with both sides. These intermediaries are correspondent banks, and they charge a handling fee for passing the funds along.

The Nostro charge is that handling fee. It is not set by your bank, which is exactly why it feels invisible: your bank quotes its own fee upfront, but the intermediary deductions happen after the money leaves, out of your bank’s control and off your original receipt.

Nostro Charge vs Your Bank’s Transfer Fee

The two are separate costs that both sit on one transfer. Your bank’s transfer fee is the flat charge your bank levies to initiate the wire, quoted before you pay. The Nostro charge is levied by third-party banks in the routing chain, deducted while the money is in transit.

The practical difference is visibility. You can see and compare bank transfer fees before sending. Nostro charges are harder to predict because they depend on how many intermediaries the payment passes through, which varies by currency, destination, and the banks involved.

Who Pays the Nostro Charge

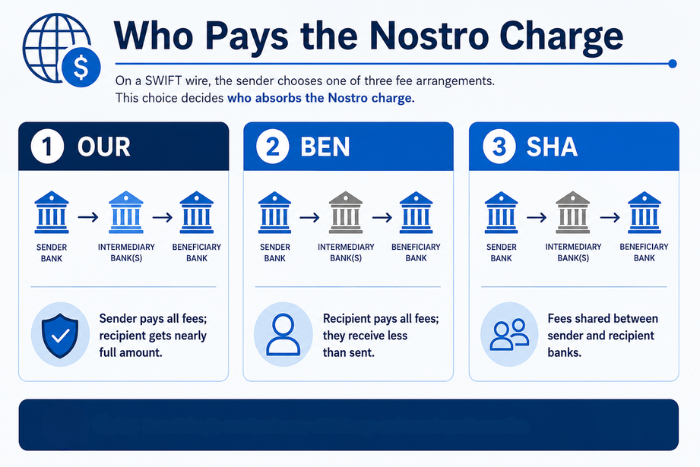

On a SWIFT wire, the sender chooses one of three fee arrangements, and this single choice decides who absorbs the Nostro charge (Banks that have moved to the newer ISO 20022 format show these as DEBT, SHAR, and CRED, but the meaning is identical).

1. OUR

The sender pays all charges, including the intermediary fees. The recipient receives close to the full amount you intended. OUR eliminates intermediary deductions; the beneficiary’s own bank may still levy an inward remittance charge. This costs the sender the most upfront but is the cleanest option when the exact received amount matters, such as tuition or a fixed invoice.

2. BEN

The beneficiary pays all charges. Every fee, including Nostro deductions, is taken from the transferred amount, so the recipient receives less than you sent. Cheapest for the sender, but the shortfall lands on the recipient.

3. SHA

Charges are shared. The sender pays their own bank’s fee, and the intermediary and beneficiary-bank charges come out of the transfer. This is the common default, and it is why a clean USD 1,000 often arrives as something less.

A Working Example of Nostro Charges in Action

A sender in India wires USD 1,000 to a beneficiary in Germany under the SHA option. The Indian bank charges its own wire fee upfront. The payment then routes through a US correspondent bank that deducts around USD 20, and the German beneficiary bank deducts a further receiving fee.

The beneficiary ends up with roughly USD 970 to 975. The USD 25 to 30 gap is not a mistake or a bad exchange rate. It is the sum of Nostro and correspondent charges taken in transit, which the SHA arrangement passed on to the transfer amount rather than the sender.

How to Reduce or Avoid Nostro Charges

1. Use a specialist money transfer provider rather than a plain bank wire. A provider like BookMyForex selects the most efficient and cost-effective partner at its discretion, routing through partner banks.

2. Choose the OUR fee option when the recipient must receive the closest figure to the exact amount intended, so no intermediary deduction lands on them.

3. Send larger, less frequent transfers instead of many small ones, since Nostro charges are largely per intermediary and repeat every time you send.

4. Confirm the destination currency and routing before sending, because a payment converted through an extra currency hop usually collects an extra intermediary fee.

5. Ask for the total landed cost, not just the transfer fee, so the intermediary deductions are visible before you commit.

Where to Check the Real Cost

Bank wire quotes rarely show the intermediary deductions, which is where the surprise hides. The BookMyForex Money Transfer shows live interbank linked rates and a transparent total cost, so an estimate of the amount the recipient actually receives is clear before you send.

BMF publishes estimated correspondent/nostro charges by currency upfront, which is genuinely better than a bank wire quote.

Compare that landed amount against a standard bank wire for the same corridor. It is the fastest way to see how much a chain of correspondent banks would quietly take on the way.

Nostro charges are one of the least understood costs in international transfers, precisely because they happen off the receipt and out of your bank’s hands. Send through optimised routing, pick the right fee option, and the gap between what you send and what arrives shrinks to almost nothing.

About the Author

Kshitij Pandey is the Content Manager at BookMyForex with over 7 years of experience in content marketing, blogging, and social media strategy. He has worked extensively on building engaging campaigns and informative resources that help users understand forex, international money transfers, and travel-related financial services.