Sending money abroad is not one product. It comes in different forms, and picking the wrong one can cost you days or thousands of rupees. The right method depends on speed, cost, and certainty.

Most international money transfers use bank transfer rails, and SWIFT is commonly the messaging network that carries the payment instructions. You can send the same transfer through a bank or online provider. A forex card is for spending abroad, while a demand draft is now rarely used.

Forex demand drafts are now mostly obsolete since most institutions accept electronic transfers instead. Forex cards work differently, since you load your own money onto a card to spend abroad, not send it to someone else. This guide breaks down each option, what it does best, where it falls short, and how to pick the right one for your payment.

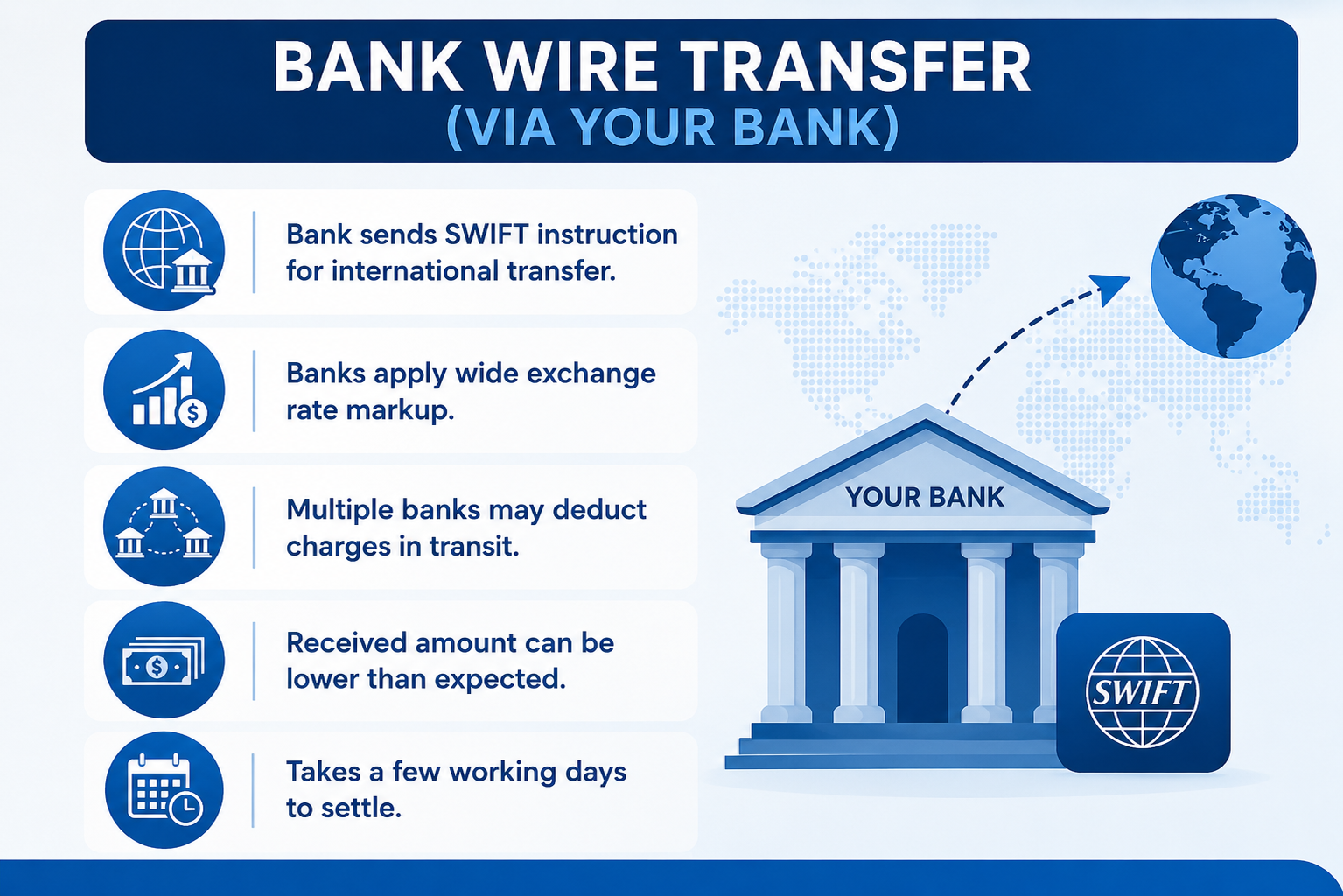

1. Bank Wire Transfer (via your Bank)

When you ask your own bank to send money abroad, the bank sends a SWIFT payment instruction, and the funds are settled through correspondent banking relationships or other payment rails.

The catch is cost, not the process itself. Your bank often applies a wide exchange rate markup. The payment can also pass through several banks along the way. Each one can deduct charges in transit. This means the amount received can end up lower than you expect.

Since more banks are usually involved, it also tends to take a few working days to settle.

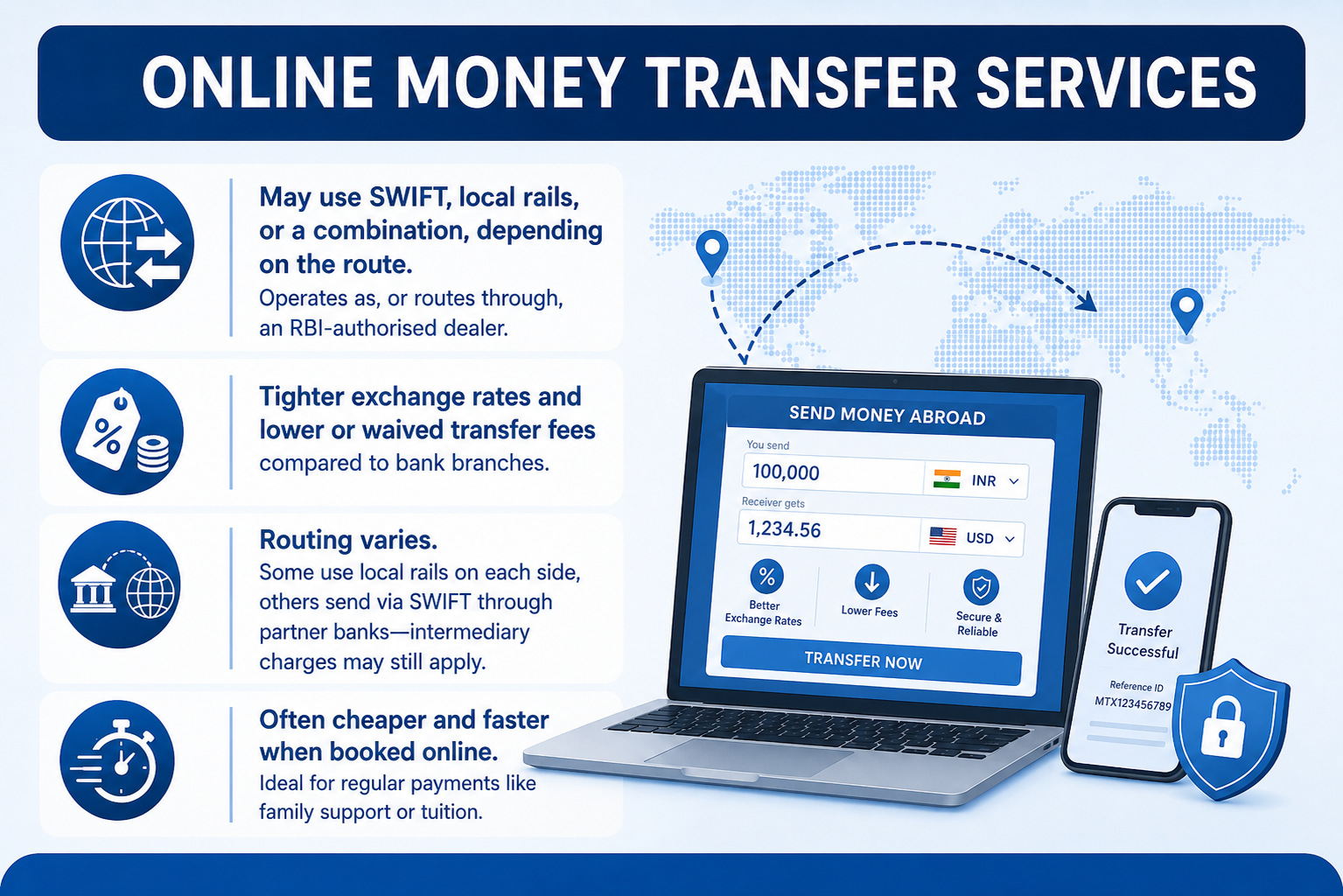

2. Online Money Transfer Services

An online money transfer may use SWIFT, local payment rails, or a combination, depending on the route. A specialist online provider operates as, or routes through, an RBI-authorised dealer.

It usually offers a tighter exchange rate and lower or waived transfer fees than a bank branch. The routing varies. Some providers settle through local rails on each side, while others send over SWIFT through partner banks, where intermediary charges can still apply in transit.

In practice, this means the same transfer often turns out cheaper and faster when booked online than through a bank branch, for the same route and the same amount. For regular payments like family support or tuition, this is usually the simplest choice.

3. Forex Demand Draft

The two are separate costs that both sit on one transfer. Your bank’s transfer fee is the flat charge your bank levies to initiate the wire, quoted before you pay. The Nostro charge is levied by third-party banks in the routing chain, deducted while the money is in transit.

The practical difference is visibility. You can see and compare bank transfer fees before sending. Nostro charges are harder to predict because they depend on how many intermediaries the payment passes through, which varies by currency, destination, and the banks involved.

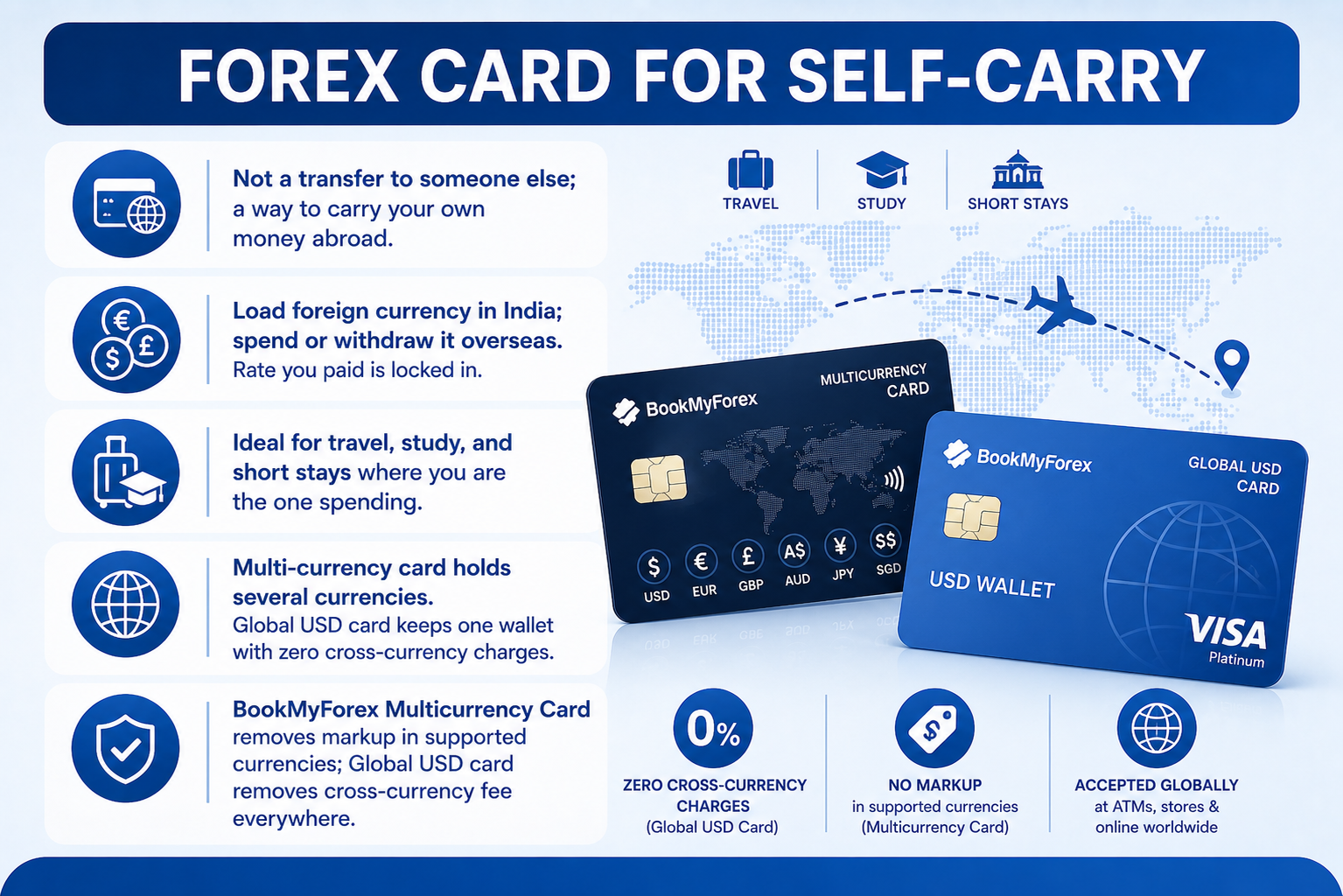

4. Forex Card for Self-Carry

A forex card is not a transfer to someone else; it is a way to carry your own money abroad. You load foreign currency onto the card in India, then spend or withdraw it overseas, with the rate you paid locked in for the currency you loaded. It fits travel, study, and short stays where you are the one spending the money.

For a traveller, a multi-currency forex card holds several currencies at once, while a Global USD card keeps one wallet with zero cross-currency charges. The BookMyForex Multicurrency Card removes the markup in its supported currencies; the BookMyForex Global USD card removes the cross-currency fee everywhere.

A Quick Comparison

A bank wire and an online transfer can both be used for international payments, but they are not always routed through the same network. One usually costs less than the other. A demand draft is an old fallback, useful only when a school or firm insists on paper. A forex card sits in a different group altogether, since the money never leaves your own hands.

| Method | Underlying process | Best for | Watch out for |

|---|---|---|---|

| Bank wire (via bank branch) | SWIFT and correspondent banking | Large one-off payments through your existing bank | Wider rate markup, extra charges in transit, slower |

| Online transfer service | SWIFT or local payment rails, routed by an authorised dealer | Regular payments like remittances and tuition | Provider reliability, though usually cheaper and faster |

| Forex demand draft | Physical paper instrument | Rare cases where an institution insists on paper | Slow, costly, risk of loss, mostly outdated now |

No single method wins at everything. The right choice depends on who receives the money, how fast it must arrive, and how much certainty you need on the final amount.

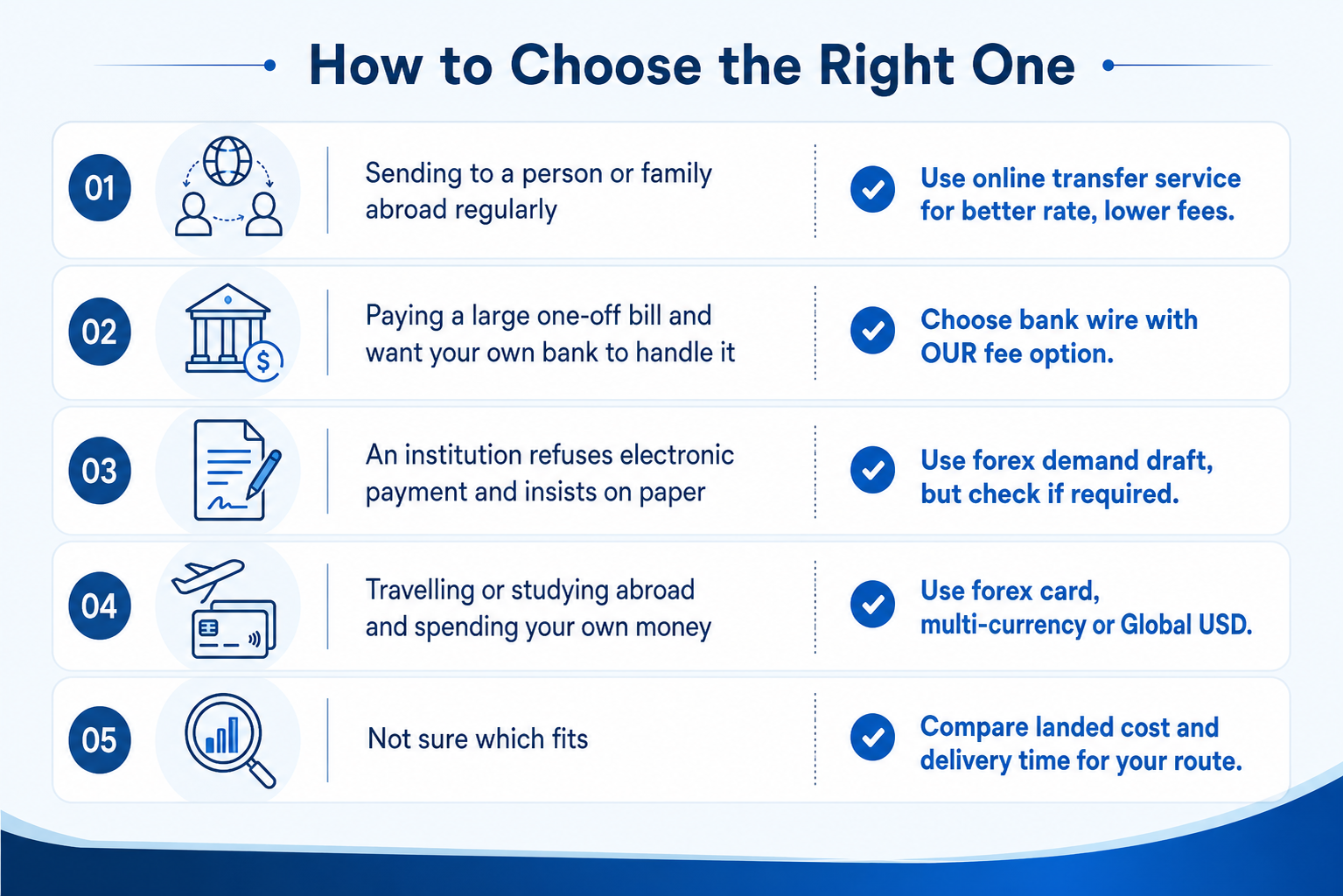

How to Choose the Right One

1. Sending to a person or family abroad regularly: Use an online transfer service. It usually delivers a better rate, lower fees, and quicker settlement than a bank branch.

2. Paying a large one-off bill and want your own bank to handle it: A bank wire, ideally with the OUR fee option so intermediary charges don’t come out of the transfer – though the beneficiary’s own bank may still deduct a small receiving fee.

3. An institution refuses electronic payment and insists on paper: A forex demand draft, though check first, since most no longer require this.

4. Travelling or studying abroad and spending your own money: A forex card, multi-currency for several countries or Global USD for zero cross-currency fees.

5. Not sure which fits: compare the landed cost and delivery time for your exact route before you decide, rather than defaulting to your home bank.

Where to Compare

The cheapest method on paper is not always cheapest after the rate markup and fees. The BookMyForex money transfer and forex card pages show live rates and transparent costs, so you can match the method to the payment and see the true cost of each.

Choosing an international transfer type is really about being honest on one question: is this money going to someone else, or is it money you will spend yourself? Answer that first, weigh speed against cost, and the right method picks itself.

About the Author

Kshitij Pandey is the Content Manager at BookMyForex with over 7 years of experience in content marketing, blogging, and social media strategy. He has worked extensively on building engaging campaigns and informative resources that help users understand forex, international money transfers, and travel-related financial services.