Remember when the dollar was just ₹45? That seems like it was a lifetime ago, doesn’t it? It got me thinking, if ₹45 seemed cheap, what was it like way back in 1947? So, I did a little research. Let’s just say the dollar has appreciated with time, and the rupee…well, not so much.

In 1947, 1 USD was equal to ₹3.30, and today it is more than ₹88. The Rupee has depreciated with time because of a variety of factors: India’s rising trade deficits, dependency on imports (mainly oil), FDI outflows, inflation rates higher than those in the US, limited export competitiveness, etc.

Let’s have a quick look at how the Indian Rupee has performed over the years and what might lie in its future!

1 USD to INR from 1947 to 2025 – A Quick Overview

| Year | Exchange Rate (1 USD to INR) | Year | Exchange Rate (1 USD to INR) |

|---|---|---|---|

| 1913 | 0.09 | 1985 | 12.37 |

| 1925 | 0.1 | 1986 | 12.61 |

| 1947 | 3.3 | 1987 | 12.96 |

| 1948 | 3.31 | 1988 | 13.92 |

| 1949 | 3.67 | 1989 | 16.23 |

| 1950 | 4.76 | 1990 | 17.5 |

| 1951 | 4.76 | 1991 | 22.74 |

| 1952 | 4.76 | 1992 | 25.92 |

| 1953 | 4.76 | 1993 | 30.49 |

| 1954 | 4.76 | 1994 | 31.37 |

| 1955 | 4.76 | 1995 | 32.43 |

| 1956 | 4.76 | 1996 | 35.43 |

| 1957 | 4.76 | 1997 | 36.31 |

| 1958 | 4.76 | 1998 | 41.26 |

| 1959 | 4.76 | 1999 | 43.06 |

| 1960 | 4.76 | 2000 | 44.94 |

| 1961 | 4.76 | 2001 | 47.19 |

| 1962 | 4.76 | 2002 | 48.61 |

| 1963 | 4.76 | 2003 | 46.58 |

| 1964 | 4.76 | 2004 | 45.32 |

| 1965 | 4.76 | 2005 | 44.1 |

| 1966 | 7.5 | 2006 | 45.31 |

| 1967 | 7.5 | 2007 | 41.35 |

| 1968 | 4.76 | 2008 | 43.51 |

| 1969 | 7.5 | 2009 | 48.41 |

| 1970 | 7.5 | 2010 | 45.73 |

| 1971 | 7.5 | 2011 | 46.67 |

| 1972 | 7.59 | 2012 | 53.44 |

| 1973 | 7.74 | 2013 | 56.57 |

| 1974 | 8.1 | 2014 | 62.33 |

| 1975 | 8.38 | 2015 | 62.97 |

| 1976 | 8.96 | 2016 | 66.46 |

| 1977 | 8.74 | 2017 | 67.79 |

| 1978 | 8.19 | 2018 | 70.09 |

| 1979 | 8.13 | 2019 | 70.39 |

| 1980 | 7.86 | 2020 | 76.38 |

| 1981 | 8.66 | 2021 | 74.57 |

| 1982 | 9.46 | 2022 | 81.35 |

| 1983 | 10.1 | 2023 | 81.94 |

| 1984 | 11.36 | 2024 | 84.83 |

| 2025 | 88.72 |

When you see this table, you would be like, “Wow, the rupee just kept going down, and nobody did anything?” But you have to remember that the situation is much more complex and, of course, much more interesting.

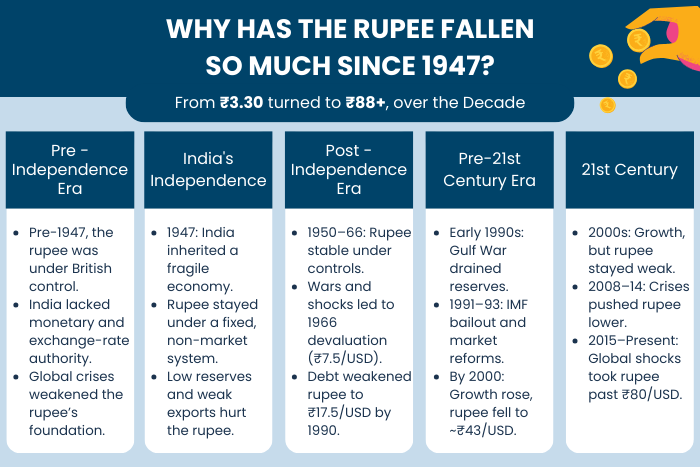

Why Has the Rupee Fallen So Much Since 1947?

To get to how ₹3.30 turned to ₹88+, we need to go through decades of history, wars, oil price increases and drastic economic changes in India. Here’s how it went down:

1. Pre-Independence Era (Before 1947)

Before gaining independence in 1947, India’s economy was controlled by British colonial policies. Naturally, this extended to the Indian rupee as well.

The rupee was not an independent currency, and it was essentially pegged to the British Pound, which itself was pegged to the US dollar within a fixed margin under the Bretton Woods system.

This also meant that India didn’t have control over its own exchange rate or monetary policies. Decisions were made in Britain, often based on its own economic needs.

So, when global economic events like the Great Depression (1930s) and World War II (1939–1945) shook the world, India was hit badly.

But since it was a colony, it had no say in how to respond or protect its currency. Massive war spending, high inflation, and disrupted trade during that time further strained India’s economic structure.

These early vulnerabilities set the stage for the rupee’s struggle in the decades to follow, especially once India became independent and had to rebuild from economic ruin.

2. India’s Independence (1947)

When India gained independence in 1947, it inherited a fragile economy. The country had just emerged from colonial rule, a devastating World War, and partition, all of which left its finances in tatters.

At that time, Indian currency began to be measured against the US dollar. The value of 1 INR then could be taken as 1 USD, considering that the national balance sheet was free from external debt or credit obligations.

However, the rupee’s value was derived from its linkage to the British Pound, which was valued at around 4 USD. Based on that chain conversion (and the older system of 1 rupee = 1 shilling 6 pence), the INR ended up being roughly ₹3.30 to a dollar.

More importantly, India had no independent monetary policy yet. The Reserve Bank of India, which had been established in 1935, was still transitioning from British to Indian control.

The country had little in the way of foreign reserves, industry, or infrastructure. With no strong export economy and growing domestic demands, maintaining a strong rupee wasn’t realistic for long.

India did not adopt a completely market-driven exchange rate. The rupee was still part of a controlled, fixed-rate system, which masked the underlying economic stress for a while, but only for a while.

3. Post-Independence Era (1950 – 1990)

From 1950 to 1966, the rupee held steady at ₹4.76 per dollar. However, this stability was more artificial than organic (supported by capital controls and limited trade exposure).

The real cracks began to show after the 1962 Sino-Indian War, the 1965 war with Pakistan and a severe drought in 1966. These events put enormous pressure on India’s economy.

Foreign exchange reserves dropped, and international lenders (such as the IMF and World Bank) pressured India to devalue the rupee in exchange for financial aid. In 1966, India officially devalued the rupee to ₹7.50 per dollar.

The 1970s brought even more challenges. The Indo-Pakistani war of 1971, the 1973 oil crisis (caused by OAPEC’s oil embargo) surged the oil prices. India, a major oil importer with low export earnings, was forced to borrow heavily in foreign currencies. This increased the external debt burden and slowly dragged down the rupee’s value.

Throughout the 1980s, India faced mounting fiscal deficits, rising inflation, and limited foreign capital inflows. The rupee weakened steadily, and by 1990, it had dropped to around ₹17.50 per USD.

4. Pre-21st Century Era (1990s – 2000)

By the early 1990s, India was in deep trouble. The Gulf War in 1990 sent oil prices skyrocketing again. India’s foreign exchange reserves dropped to dangerously low levels, barely enough to cover two weeks of imports. The country was on the verge of defaulting on its external debt.

In order to prevent collapse, India pledged its gold reserves and went to the IMF for a bailout. In return for this, it agreed to an opening of its economy. This was a major moment in India’s economic journey.

In 1991, India devalued the rupee again and launched significant reforms relating to trade liberalisation, deregulation, and privatisation. Another significant shift was the introduction of a dual exchange rate in 1992 and a transition to a market-determined exchange rate in 1993.

That means the value of the rupee would now be influenced by global demand and supply, not just government controls. Naturally, this brought more volatility and made the rupee more vulnerable to global economic shifts.

By the end of the decade, the rupee had depreciated to about ₹43 per dollar. While liberalisation improved GDP growth and attracted foreign investment, the rupee continued to weaken due to trade deficits, rising import bills, and capital outflows.

5. 21st Century (2001 – Present)

In the early 2000s, India’s economy began to accelerate, driven by a rising IT sector, foreign investments and rising exports. Yet, the rupee had very little consistent strength, still continuing to fluctuate between ₹44 to ₹48 per USD due to still relying on imported oil and hence a growing trade deficit.

However, the momentum was not entirely lost. The rupee still managed to strengthen briefly during this period, supported by steady capital inflows, rising remittances, and overall macroeconomic stability.

Then came the 2008 Global Financial Crisis. The rapid exit of foreign institutional investors (FIIs) from Indian markets, as well as the worldwide demand slump, caused a sharp fall in the rupee again. Exports decreased, stock market prices fell, and investor sentiment weakened.

In the subsequent years, global markets began to recover, but the Indian rupee remained under pressure due to persistent trade and ongoing current account deficits. The period 2011-2013 was particularly difficult for us.

Global crude oil prices remained high, gold imports increased, and India’s current account deficit widened to over 4% of GDP. Overall, this led to currency depreciation with the INR falling to nearly ₹60+ per USD by 2014.

After 2014, a series of domestic policy measures aimed at economic reform, including Make in India, Digital India, and GST rollout, were introduced, which surely opened up channels for increased foreign investment.

However, external actions continued to signal a reduced momentum. Interest rate hikes by the US Federal Reserve, as well as fluctuations in global oil prices, seemed to pressure the rupee, compounded by unilateral trade policies from major economies. By 2018, the rupee slipped to ₹70 per USD.

The 2020 pandemic was another significant blow, with lockdowns, export restrictions, lowered GDP, and overall uncertainty leading to the rupee falling to record lows. Yet again, in an unexpected twist of fate, India’s forex reserves crossed $600 billion for the first time, providing a much-needed buffer.

But then came the Russia-Ukraine war, global inflation, and aggressive rate hikes from the US Fed, all of which created havoc in emerging economies in 2022 and ultimately pushed the Indian rupee past the ₹80 mark to the dollar. Nevertheless, during the worst part of the global uncertainty, India was, on the whole, relatively less impacted than many emerging economies.

India’s resilience continues to stand out. The challenges remain, such as trade imbalances and geopolitical shifts, but India is still among some of the fastest-growing economies in the world, driven by strong domestic demand, a digital-first approach, and an expanding manufacturing base.

What Lies Ahead for the INR vs USD?

While predicting exact exchange rates is tricky, we can surely read the signs. Here’s what could shape the future trajectory of the Indian rupee:

1. India’s Domestic Story Is Getting Stronger

From digital public infrastructure to a blossoming startup ecosystem, there is tremendous domestic momentum in India. An improving ease of doing business, rising consumer demand and a renewed push for manufacturing could enable the rupee to strengthen gradually.

2. But Global Headwinds Aren’t Going Away

The US Fed’s rate decision, oil prices, geopolitical tensions and the dollar index (DXY) would still leave a negative influence on the rupee.

3. Rupee May Not “Appreciate” Significantly, But Could Stabilise

While the rupee is not going to snap back to ₹60 levels, there is a possibility of a range-bound rupee (say between ₹80-83) and a relatively stable rupee, if India’s real economy remains robust and exports become better.

4. The Make-in-India Effect

While the dollar’s dominance isn’t going away soon, if India can find a way to lessen its import dependence on oil and electronics, and eventually evolve into a net exporter of high-value goods, the rupee has the potential to gain long-term strength.

5. More INR-Based Global Trade

India’s deals with countries to settle trade in rupees could gain momentum. If more nations accept INR for trade settlements, it might boost rupee demand globally and reduce dollar dependency (slowly, but surely).

6. Capital Flows & Investor Sentiment

FII/FDI inflows are important. Strong corporate earnings, political stability, and global trust in India’s digital economy could attract capital. But capital outflows during uncertain times can disrupt the stability of the Indian rupee’s value relative to the dollar.

7. The RBI Will Remain the Gatekeeper

The Reserve Bank of India will continue to intervene to regulate extreme volatility from potential capital inflows and/or outflows. However, don’t expect free floats to and from certain real-time values, especially around politically and economically sensitive transitions.

About the Author

Bhawna Nijhawan is the Content Manager at BookMyForex and the go-to person for creating engaging, informative content that resonates with the platform’s diverse audience. With over 8 years of experience in content writing and more than 4 years in the forex industry, she knows exactly how to simplify complex forex topics into something everyone can relate to.